Imperfect Replication Beats Single Manager 9/10 Times

Subscribe to Our Blog

When the two are compared, it seems evident that the downside risk of investing in high cost, tax-inefficient single manager investments outweighs the model error of a low-cost, tax-efficient replication. Working through the numbers, it looks like replication could be about 9x more likely to outperform single manager investments over time.

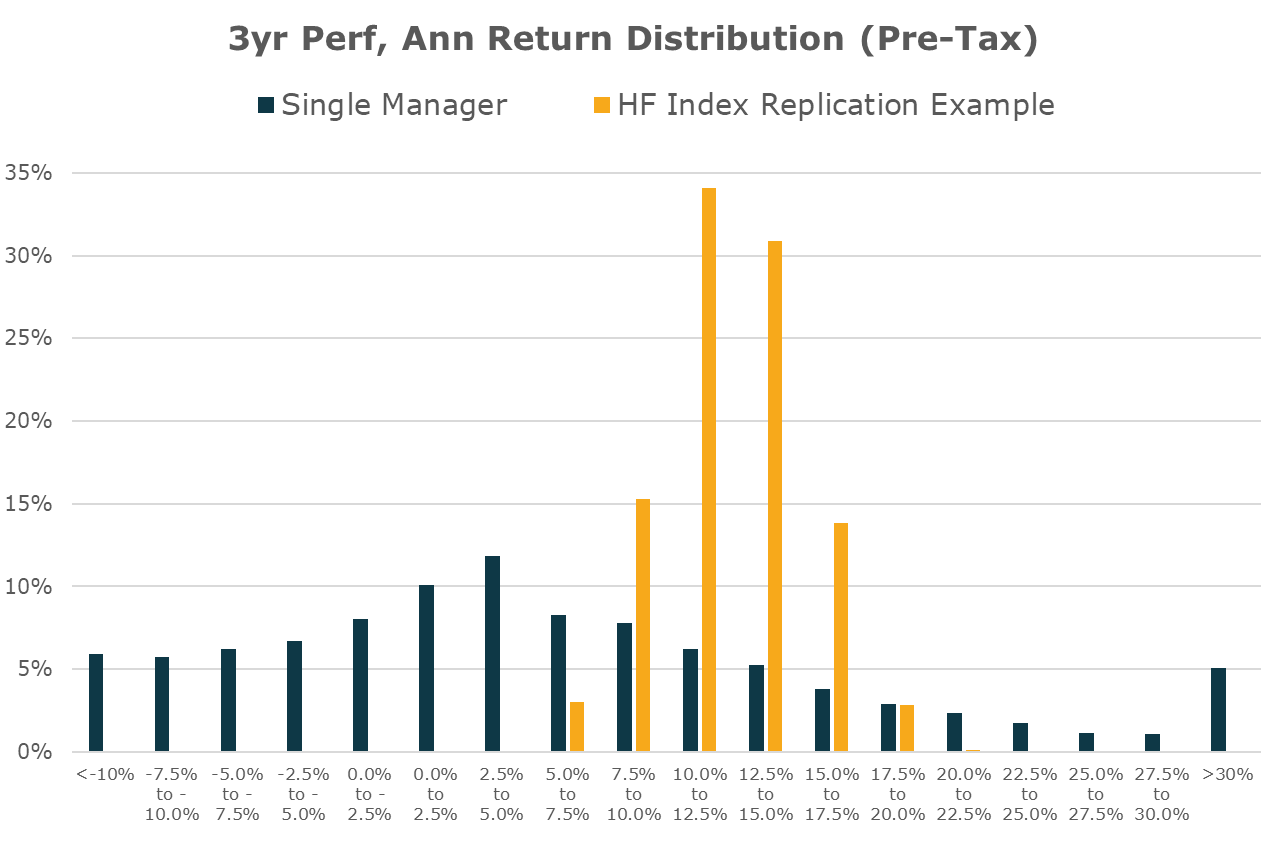

To get a tangible sense of the trade-off between these choices, we compared the range of outcomes over the last 3 years between:

(1) the actual distribution of the net of fees returns of approximately 3000 single Hedge Fund managers (Source: Preqin)

(2) the estimated range of a Hedge Fund index replication strategy targeting the gross of fees index returns with a roughly 3% error standard deviation and 1% fees.

While the replication is imperfect, the range of its return is narrower and the median outcome is a few hundred basis points higher. In roughly 70% of the possible head-to-head outcomes of a randomly selected head-to-head comparison, the replication outperforms the single manager approach.

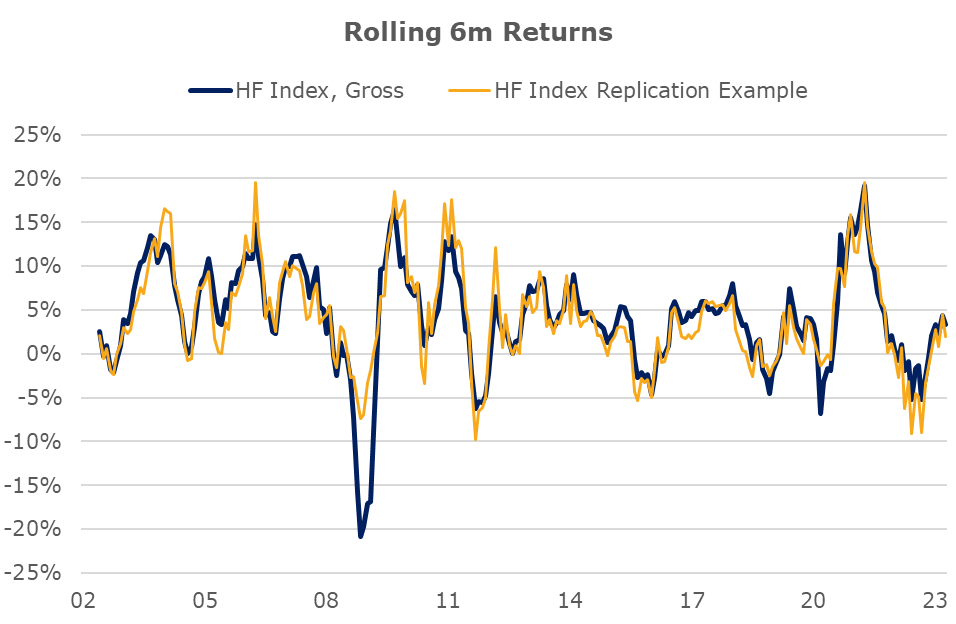

It can be hard to intuitively picture the assumed tracking error from the above, so the chart below shows an example replication strategy that exhibits a similar type of modeled variance on a 3yr time frame. To align more with shorter-dated evaluation periods, we show the rolling 6m returns. The replication example is not perfect, but it tracks effectively. While the quality of replication in the future can’t be measured, what is shown is in the range of what is plausible using today’s technologies.

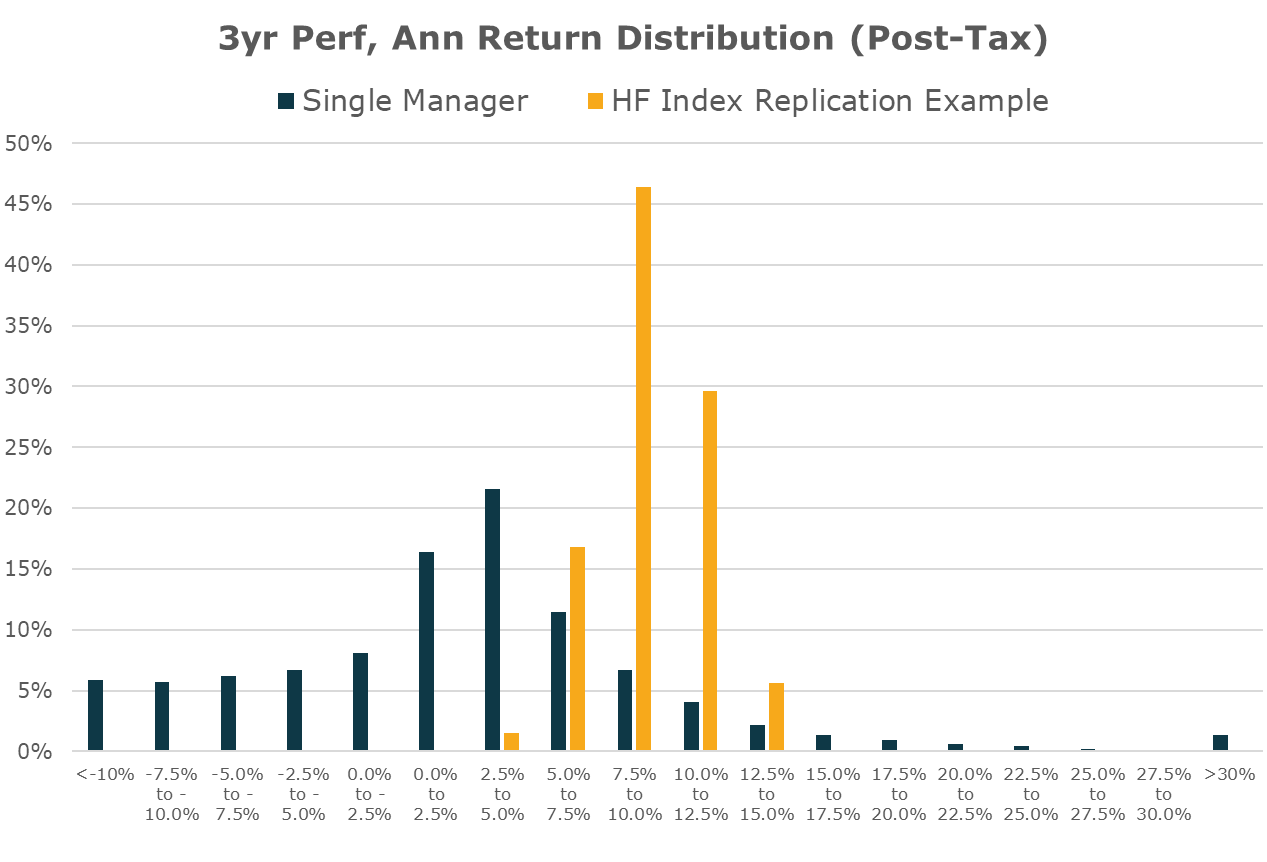

One of the advantages of modern Hedge Fund replication approaches is that they can be packaged in a much more tax-efficient ETF structure rather than typical LP structures. While every circumstance is different, below we assume that the replication tax structure is 25% based on capital gains and the single manager tax rate is 50% based on marginal income tax rates.

Accounting for the relative tax consequences increases the head-to-head outperformance of the imperfect Hedge Fund replication vs. the single manager LP positions to nearly 85% of the outcomes.

Most investors face the additional hurdle of being able to actually get into the very best funds either because they are closed, difficult to identify, or because the minimums are too high for even relatively well-off accredited investors. Even assuming a third of the funds in the right tail were uninvestable for one of these or other reasons suggests that by choosing an imperfect hedge fund replication strategy odds are 90%+ of outperforming single manager selection over a time frame of a few years. And that doesn’t consider any of the work required to make single manager investments - diligence meetings, paperwork, ongoing Schedule K-1s, etc.

Ultimately, you could conclude that while with a single manager there is the *possibility* of achieving higher returns than with a Hedge Fund replication strategy, the *probability* of achieving a better outcome supports investment in replication. The combination of single managers producing a wider distribution of returns with burdensome fee drag and negative taxes impacts results in a distribution that seems in its totality less attractive.

In investing the opportunities to raise your probability of a better outcome by as much as 10x are scarce. That opportunity now presents itself, as low-cost, tax-efficient ETF offerings have emerged in recent years. Despite this possible risk-reward, only about 0.06% of money invested in Hedge Fund strategies are currently in low-cost replication ETF structures.

For informational and educational purposes only and should not be construed as investment advice. The historical analysis discussed herein has been selected solely to provide information on the development of the research and investment process and style of Unlimited. It does not constitute an offer to sell or a solicitation of an offer to buy any security. Opinions expressed are our present opinions only. The material is based upon information which we consider reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. The historical analysis should not be construed as an indicator of the future performance of any investment vehicle that Unlimited manages. No investment strategy or risk management technique can guarantee return or eliminate risk in any market environment. No Representation is being made that any investment will or is likely to achieve profits or losses similar to those shown herein.